How to BUSINESS Analyze Stakeholder Requirements

Many BAs ask me where to get the business requirements when no one has done Enterprise Analysis or even a simple “Business Knead”. “That stuff is above my pay grade”, they say, “and even if it weren’t nobody gives us enough time or information about what is really going on. We barely have time to clean up today’s mess, never mind tomorrow’s.”

Many BAs ask me where to get the business requirements when no one has done Enterprise Analysis or even a simple “Business Knead”. “That stuff is above my pay grade”, they say, “and even if it weren’t nobody gives us enough time or information about what is really going on. We barely have time to clean up today’s mess, never mind tomorrow’s.”

“Me three” is my reply. My experience and certification don’t change basic human nature. Even when I am invited to high-level meetings, no one thinks of me as a “business owner” or manager. The checks are written above my head, and many command structures still insist on top down flow only.

Stick with us (thanks to my anonymous class, who inspired months of blogs) as we transcend BABOK by explaining how (and why) to get something from nothing , and in the process raise your pay grade*.

Last month we tried to use ordinary analysis to break down stakeholder requirements driven by the need to cut costs, resulting in something like:

1. Internal Service Costs

- Total Costs of Internal Service by Organizational Structure

- Costs by Service Provider Department

- Costs by Service Provider Team

- Costs by Service Provider (???time/effort)

- ???Other incidental costs (overhead/supplies)

- ???

- Costs by Service Provider Team

- ???Costs by Service Recipient Department

- ???Costs by Service Recipient Team

- ???Costs by Service Recipient (time/effort)

- ???Other incidental costs (overhead/supplies)

- ???

- ???Costs by Service Recipient Team

- Costs by Service Type

- ??? On boarding

- ??? Annual Training

- ??? IT Help Desk

- ??? HR Guidance

- ??? More…

- Costs by Chances to Save Resources

- ???

- ???

- More ???Cost Views…

- ???

- ???

- Costs by Service Provider Department

2. ???Internal Service Benefits

- ???Etc.

- ???Left as an exercise for the reader, similar to above yet different.

I was so tempted to expand this list of trees**, but I decided to take a peek at the forest instead. Why?

Although we have tried to expand the original stakeholder requirement, it is still unclear what is or isn’t a priority. The focus so far seems to be on WHO DID WHAT. The BABOK says that BAs have general business knowledge. What do you know about measuring or enhancing employee performance? What are the impacts of singling persons or departments out? Short term? Long term?

It is not clear how knowing how much internal service is being done by whom for where will change costs or improve the business. At best we could decide to re-train (or fire) the lowest performers, and we will discover that (by definition) there aren’t many of those, and once fired, someone else will take their place. There might be a few VERY high performers, but they will not be reproducible as a general rule.

How many Michelangelos does it take to screw in a light bulb? How many non-Michelangelos does it take to paint a masterpiece? It is quite likely that most employees are doing the best they can in the circumstances, with statistical fluctuations over time, but no significant performance differences.

Blaming (even identifying) the workers to reduce costs is an organizational dead end. Many great leaders reject the use of the “Theory X” approach” (workers are lazy thieves who are best motivated by whippings and emotional abuse). These include Robert Townsend of Avis (“Up the Organization” remains relevant to this day), Douglas McGregor of MIT, and especially Edward Deming (“brought to you by the nice people who made your nice car that you can rely on”) among MANY other quality triumphs. Deming showed that in most cases job performance is randomly distributed among employees over time, once inputs, policies and tools are established.

Another high-level concept worth knowing is that the tyranny of numbers is a risk in any project (“Hey, we are paying $10 per bug found!”). Cutting costs is not a business goal by itself. If it were, the best approach would be to cease operations entirely, achieving zero costs. Finance mavens will recognize that investing zero has “opportunity costs”, and there is no way out – figure out how best to use resources, or stick them in your mattress to rot.

This makes us realize that the stakeholder requirements are not remotely robust or useful as imagined. They represent a literal attempt to monitor internal service costs, perhaps in an attempt to “be fair” and “spread the pain”, with no clue how these costs relate to the business success.

If we pursue such requirements, we are likely to create a system to track internal service costs that has little or no impact on the quality of decision-making. Worse, it might have too much impact on the quantity of decision-making (“look, department D is giving too much internal service this month, let’s dock their pay to re-motivate them to reduce the service”).

SO, what is the real business need? Cost control obviously matters, but how does that “high level abstract not quite a requirement as stated” relate to possible actual requirements? Let’s use a “MOST” analysis (Missions, Objectives, Strategies, Tactics) and see if it helps:

Let’s agree (for this blog) that many organizations have “high-level” missions that are a little “generic”; something like:

Be Customer Driven

Make Quality Everyone’s Business

Practice Respect For All

Maximize Efficiency, Effectiveness and Profitability

This may seem fluffy and devoid of substance (it is** :)), but we can use it as a starting point to re-imagine the stakeholder requirements. It would seem that the mission to “Maximize Efficiency” is the primary mission in play. Leaving out “Profitability” is the easy to commit error. When I trace to this level some PMs (not you, not you, resemblance to real people is a coincidence) tell me “everyone already knows that, don’t waste your time.” In spite of any resistance, no one can forbid me to know the organization mission, and use the knowledge to add value to stakeholders.

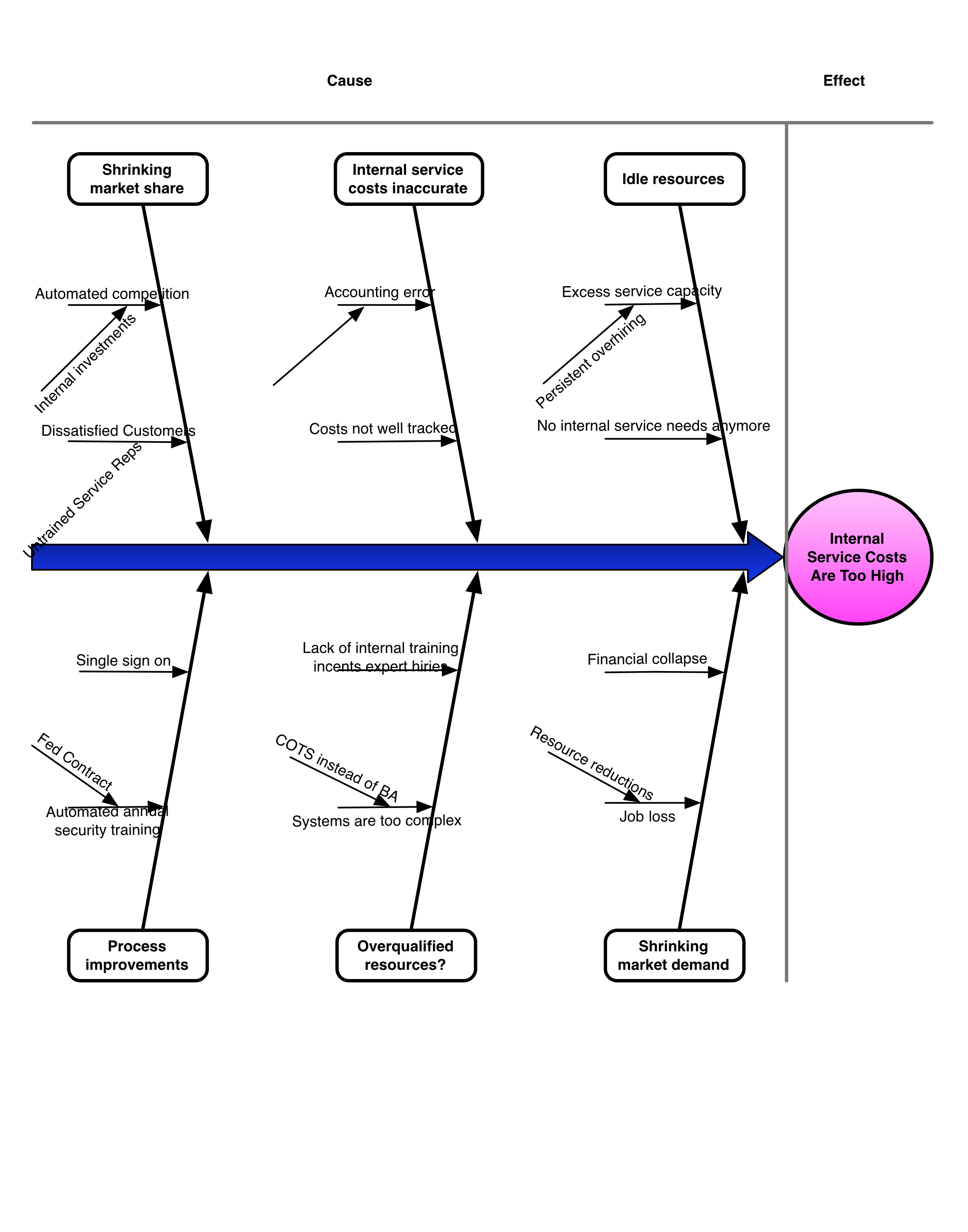

This seems like pure “Root Cause” business need stuff. Root cause stuff can be sensitive to discuss, and requires tremendous diplomacy, facilitation and values (don’t blame people) to do well. That is a different essay for some other day. In an attempt to work with this group of “internal service” stakeholders we will pretend to analyze the reasons that internal service is TOO costly: Click image to view larger.

Click image to view larger.

OOPS! Depending on the actual root cause analysis (mine is made up for the blog, can you spot the big error?) cutting internal services might hurt effectiveness and profitability.

What would you do? Don’t hold back, the future of the organization will be impacted one way or another.

Hmmm…is the problem the root cause analysis, or is there a deeper problem? What is the root cause of this rather un-useful root cause analysis? WHO CAN OFFER AN ANSWER? Will James marry Oneida or stay in Paraguay? Is anybody out there?

Have fun!

* Pay grade ≠ pay amount – negotiation is a key competency and worth a try :).

** Not ! 🙂

*** A higher quality mission statement might be “Balance efficiency, effectiveness and profitability”. Maximizing everything sounds good (and seems simple) yet is just as hard as “Balancing”. The word “Balancing” does not hide the deeper truth that tradeoffs are usually necessary and too much simplicity can mislead.

Don’t forget to leave your comments below.